The Scenario

An individual owes you a debt (which is unsecured), such as a debt for non-payment of goods purchased.

- The individual enters into bankruptcy.

- You have not been notified of the individual’s bankruptcy but have a “provable” debt.

- 3 years later, you are now aware that the individual is a discharged bankrupt (the Discharged Bankrupt).

Can you demand payment if it was an unsecured debt?

Generally, ‘No’ – the Discharged Bankrupt will no longer be liable to pay debts that are deemed to be covered under the bankruptcy rules for certain debts. Usually after three years a bankrupt will ultimately be discharged from bankruptcy and released from their liabilities owed as at the date of bankruptcy.

On this basis, you will not be able to demand payment of the debt, and the individual is not liable to repay the debt (if the bankrupt failed to disclose a debt owed at the time of bankruptcy, they may be liable to prosecution by Australian Financial Security Authority, but that would not recover the debt).

Debts included and not included in Bankruptcy

Debts included in bankruptcy include unsecured debts (being, tangible debts), examples of which may include, but not limited to:

- Credit and store cards;

- Unsecured personal loans;

- Unsecured business loans;

- Utility bills (ie electricity, phone etc); and

- Medical, legal and accounting fees.

Conversely, debts not included in bankruptcy include, but not limited to:

- Debts incurred after the bankruptcy begins;

- Unliquidated debts (these are debts where the amount of debt is yet to be determined, not arising from contract, promise or breach of trust, which is quite rate); and

- Child support and maintenance debts.

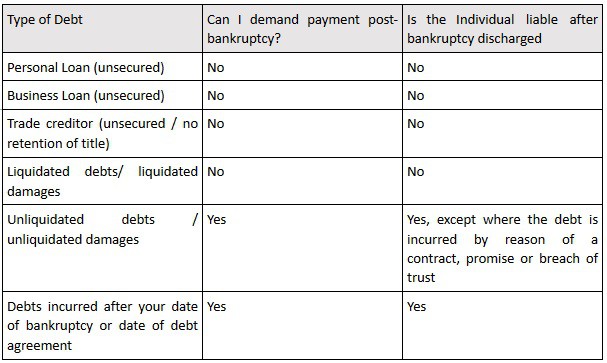

Below is a comparison table of examples of debts that may and may not be recoverable post-bankruptcy.

How do I recover an unsecured debt in this scenario?

Generally, the only way to recover an unsecured debt is if you are a named creditor with a provable debt that came about before the start of the bankruptcy. Provable debts are debts and liabilities, present and future, certain or contingent to which a bankrupt was subject at the date of the bankruptcy, or to which they may become subject before their discharge by reason of an obligation incurred before the date of the bankruptcy.1

If your debt is a “provable debt”, you would be able to participate in the bankruptcy and be entitled to repayment of your debt, in whole or part.

However, in this Scenario, you are not a named creditor that have not been notified of the bankruptcy, you may be hindered in recovering the debt. Conversely, if you are able to prove that the debt was incurred after the bankruptcy, the individual will be liable, and you would be able to pursue the individual for payment.

Accordingly, the best avenue in which to recover an unsecured debt is to stay informed with respect to the financial position of the individual who owes you the debt.

How can we help?

If you are unsure of whether you can make a claim for an unsecured debt against a discharged bankrupt, please contact the Corporate and Commercial Lawyers at Rostron Carlyle Rojas Lawyers on (07) 3009 8444 or email us at [email protected].

Please note the contents of this article are for general purposes only and does not by any means constitute legal advice, or should it be relied upon.